What is CKYC and why is it important?

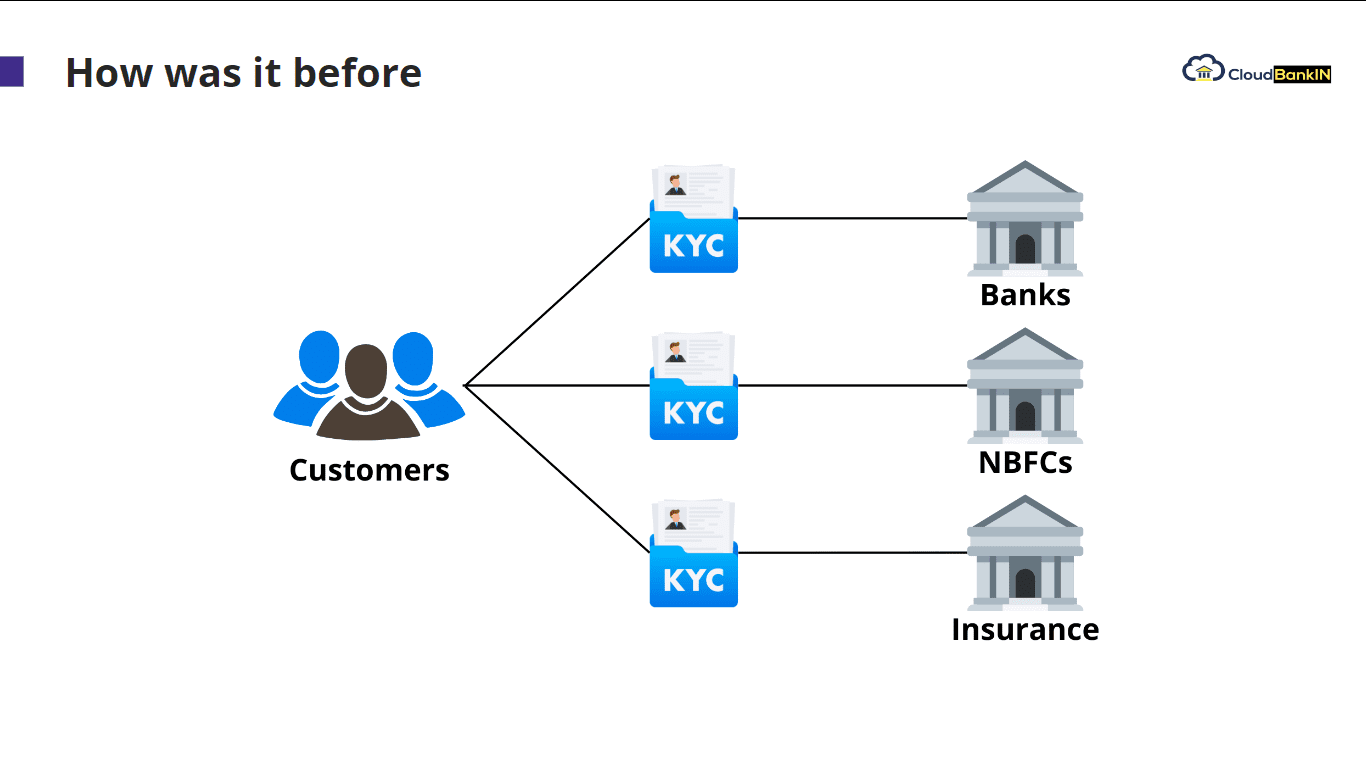

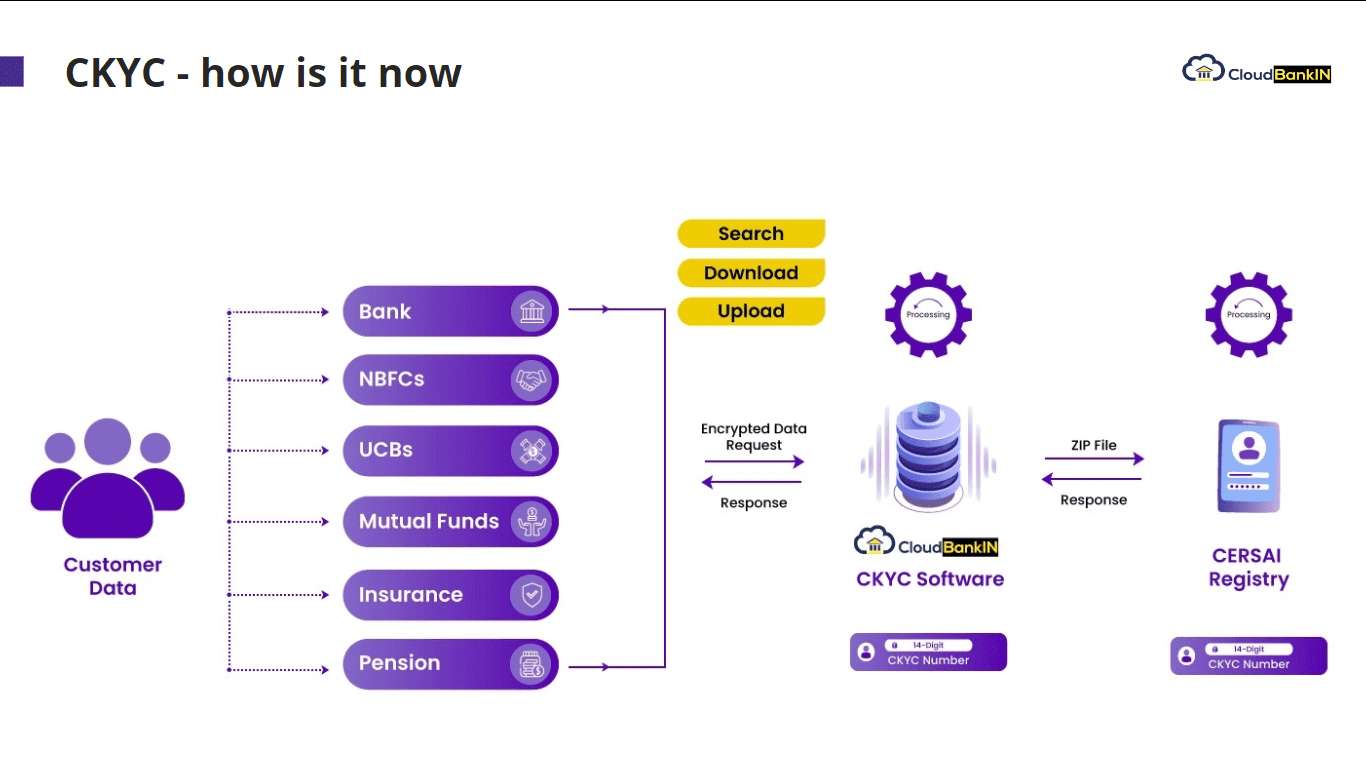

CKYC, or Central Know Your Customer, serves as a centralized repository for KYC data. Before its implementation, customers had to submit separate KYC documents to each financial institution they interacted with. This often led to inconsistencies and outdated information. With Central Know Your Customer initiative, once a customer’s KYC data is submitted to any financial institution, it’s pushed to the CKYC registry. Other institutions, with the customer’s consent, can then pull this data, ensuring they always have the most up-to-date information.

A CKYC software solution sits in the middle of this process, facilitating the request and response of this data through APIs. This centralization has several benefits:

- Alternate to Aadhar: Many financial institutions now use CKYC process as an alternative to Aadhar for KYC verification. This is especially useful when the Aadhar mobile number isn’t mapped or when the Aadhar server is down.

- Multiple Valid Documents: CKYC system accepts various valid documents, including Aadhar, PAN, driving license, and voter ID. Once a customer’s data is in the CKYC registry, institutions can retrieve the information using any of these IDs.

- Ease of Use: CKYC server provides a more stable and user-friendly experience compared to other systems.

- Inter-usability of KYC records across financial institutions.

- Reduce the burden of constantly producing and verifying KYC for a new financial institution.

Functionalities of CKYC

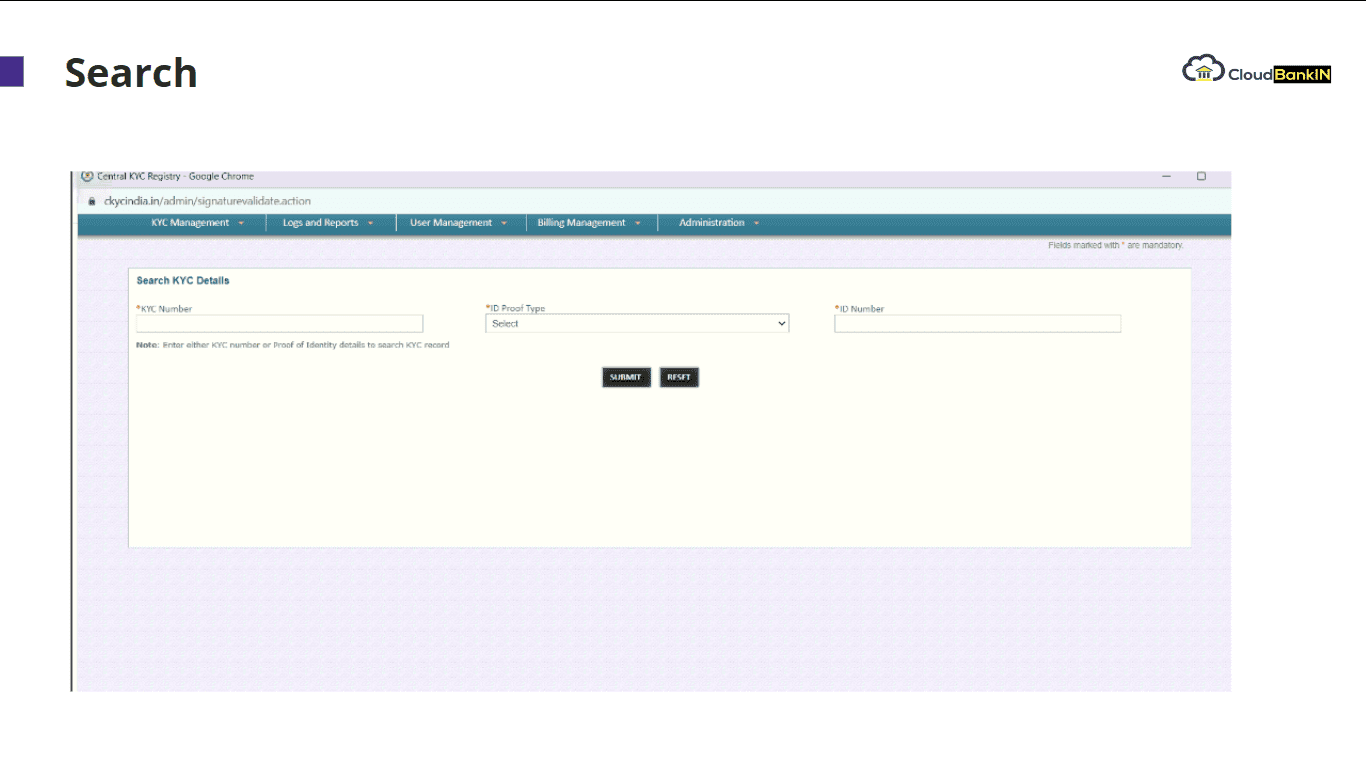

Search

This function allows institutions to search for a customer’s CKYC number using various identification numbers, such as PAN. By inputting the PAN number, institutions can retrieve the CKYC number along with some personal details like name, father’s name, and mother’s name.

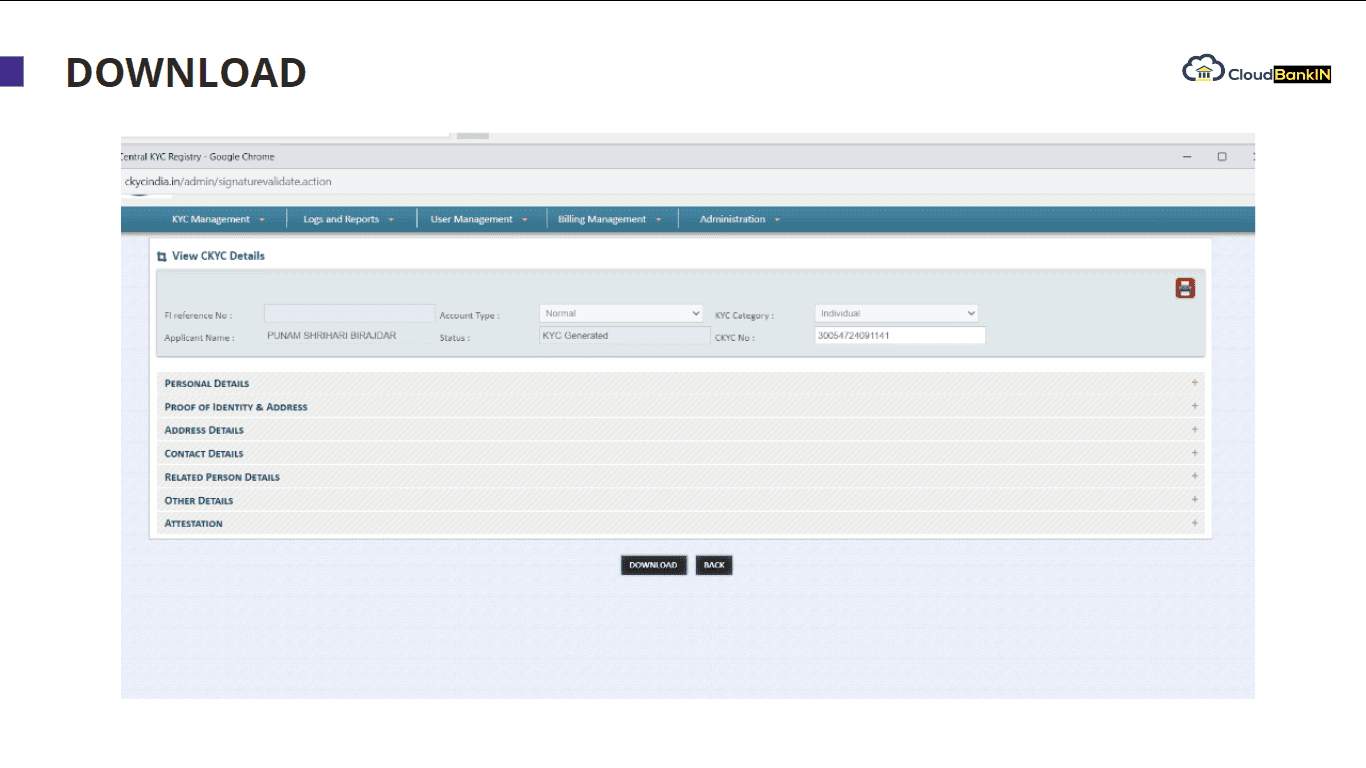

Download

Once the CKYC number is obtained, institutions can use the download function to retrieve all the information submitted by the customer during their CKYC registration.

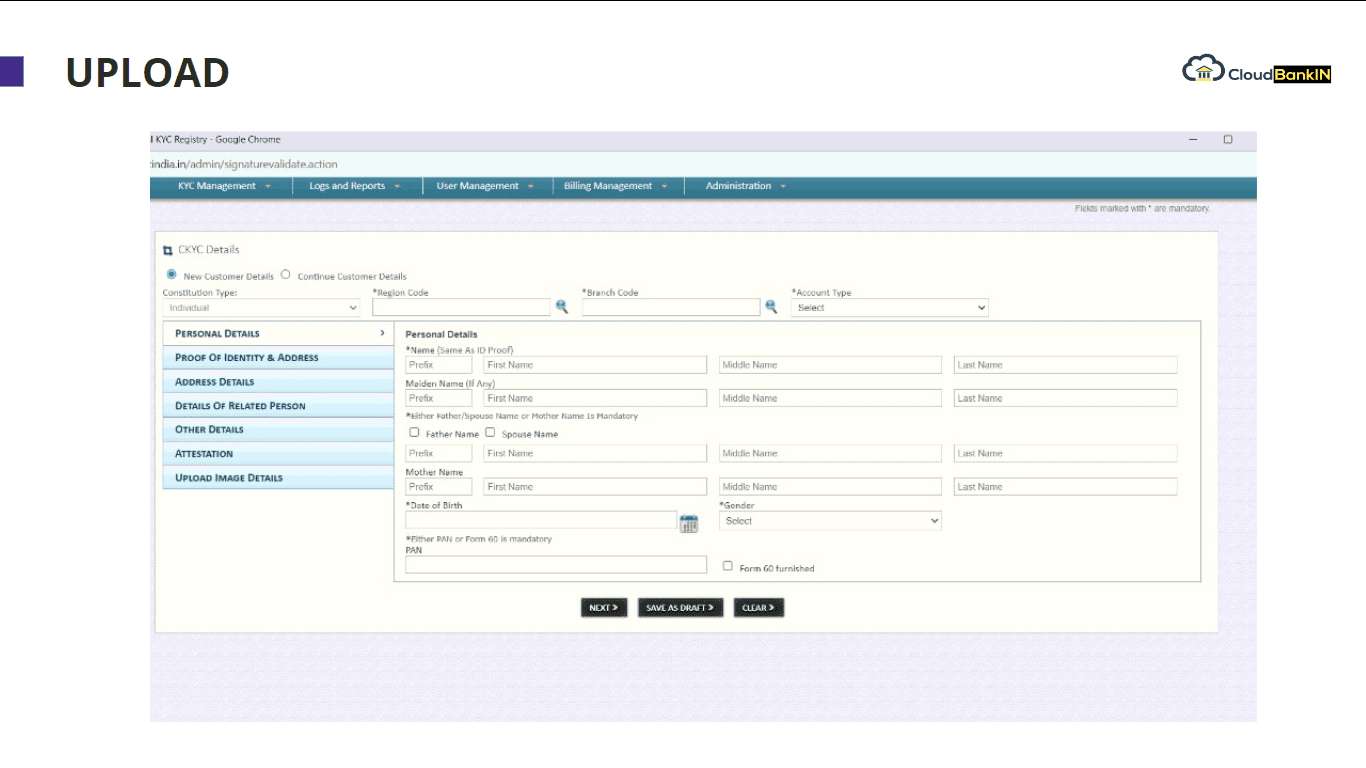

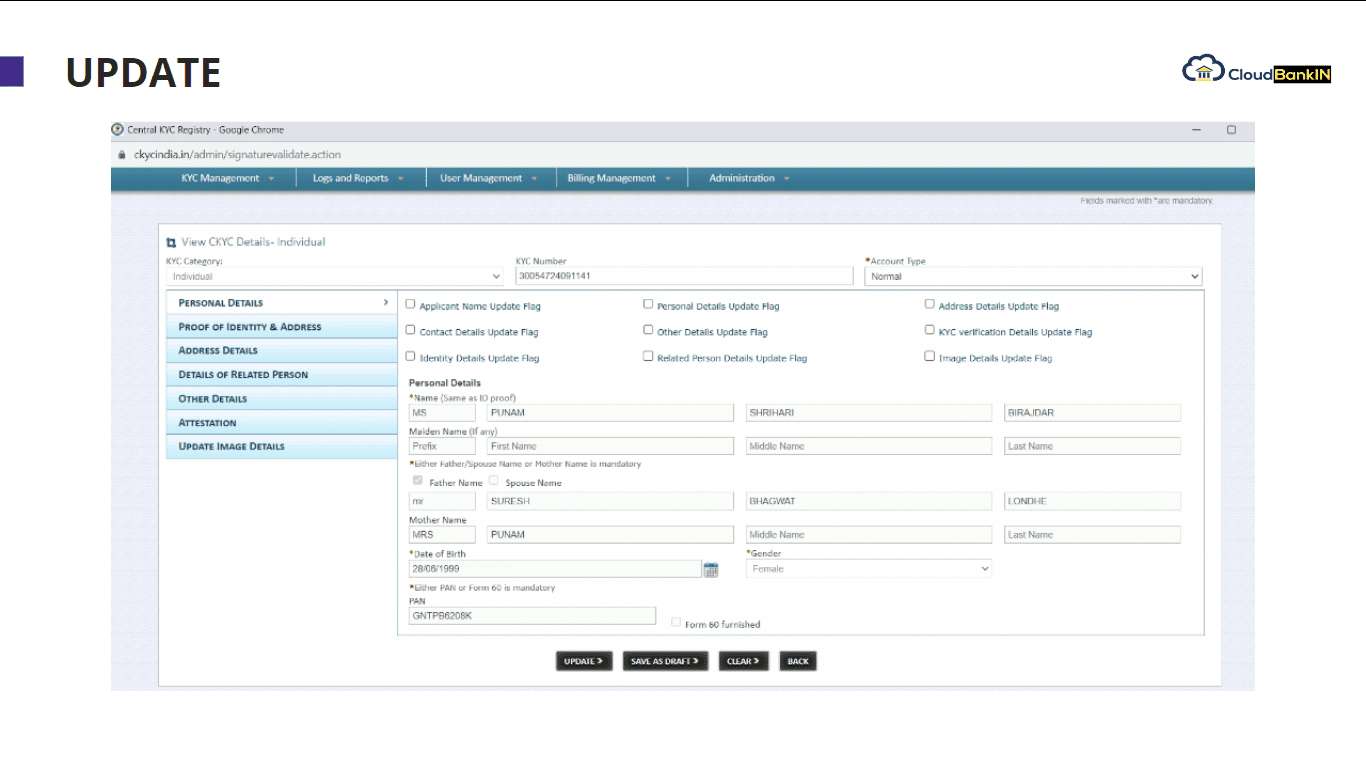

Upload

There are two main functionalities under upload:

- New User Creation: Institutions can create a new CKYC record by filling in various sections like personal details, address, related person details, and other relevant information.

- Update Existing User: If a record was created by the same institution, it can be updated directly. Otherwise, the record must first be downloaded before any updates can be made.

Related Post

How Lending Companies can disburse the loan in 10 mins

Technology has woven its magic in the 21st century across

Navigating Through The Regulatory Compliances for NBFCs

Overview Regulatory compliance for Non-Banking Financial Companies (NBFCs) has undergone

10 Powerful Tools To Help Automate Your Lending Process

In a fast-paced, competitive world of the lending industry, financial