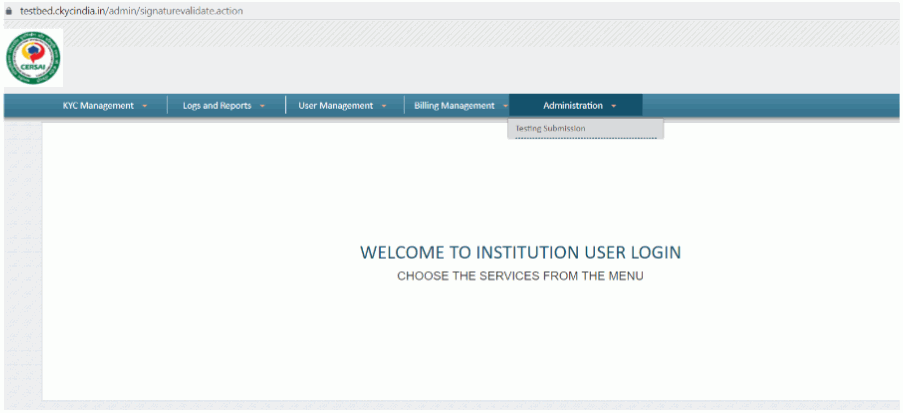

(Image Credit: Testbed CKYC)

The above screenshot will appear after entering the login test-bed credentials.

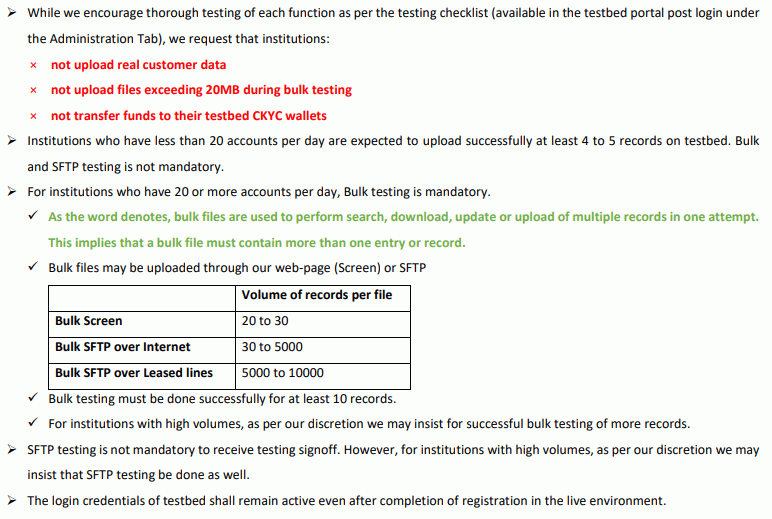

The Overall Gist of Carry-Out Testing:

Financial institutions are required to add a minimum of five test or dummy customer records. These records should include parameters such as First Name, Middle Name, Last Name, Date of Birth, Marital Status, Family Details of Father & Mother (First Name, Middle Name & Last Name), Full Address, and Identification Details (like Aadhar, PAN, etc.), Identification Proof Documents (either in PDF format or a screenshot), etc. The data can be entered manually or uploaded as a ZIP file by the financial institution. The customer record may consist of 100+ different parameters, depending on the specific requirements of each institution.

The first stage of verification, known as maker-level verification, involves basic validation checks. This step validates the input details provided by the institution. For instance, checks are made to ensure the Aadhar Number entered is a valid 12-digit number, that the attached Aadhar document doesn’t exceed 250 KB, and that in case a ZIP file is uploaded, its validity is confirmed.

The process then advances to the second stage of verification, known as checker-level verification. This stage ensures the functionality of the CKYC processes (upload, search, download, and update) is working as intended. The goal here is to confirm that the customer details provided by the financial institution are accessible on the CKYC portal. For example, if a customer’s Aadhar information is input, the system checks whether that data is available or not.

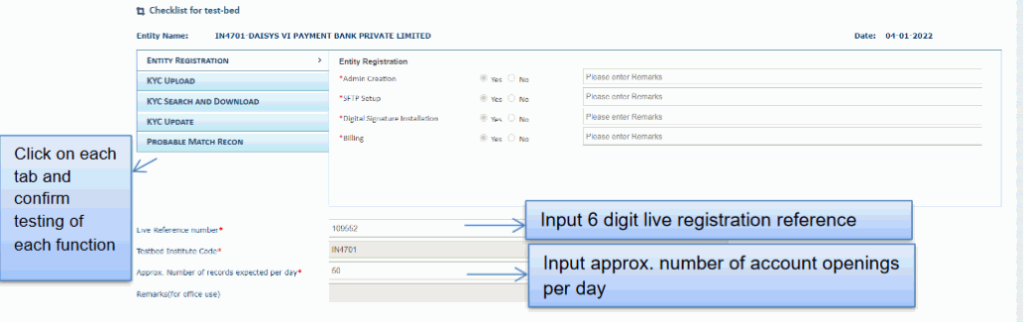

Checklist for Test-bed: