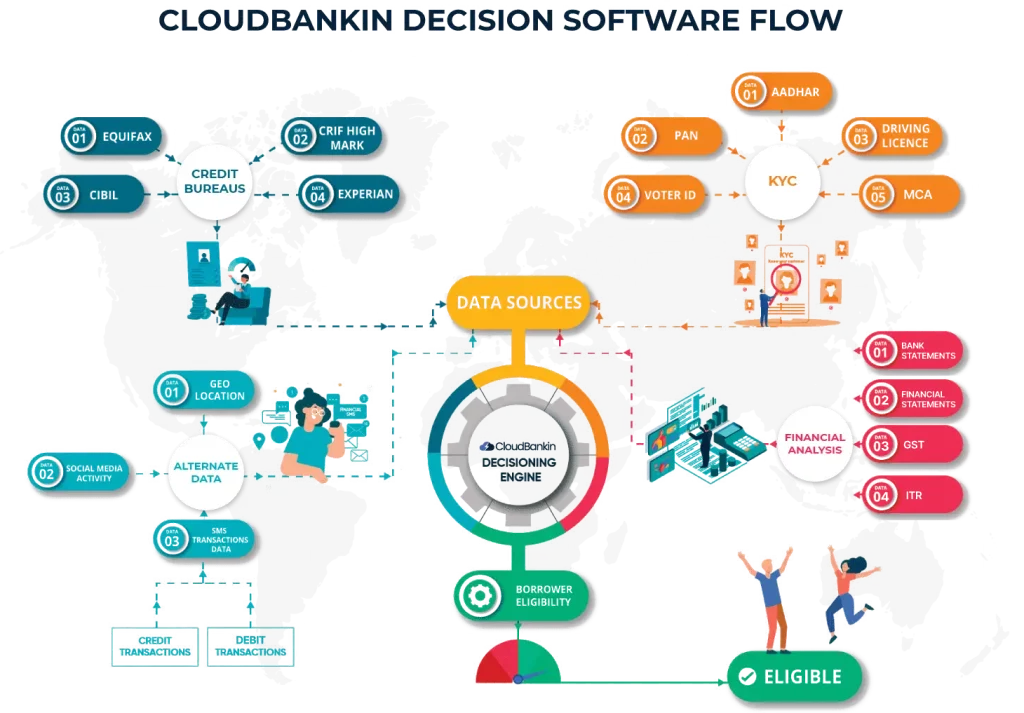

| Aadhar | Aadhaar number | Name, Address, DoB, Gender, and Photograph linked to Aadhaar | Unique Identification Authority of India (UIDAI) | Helps to ensure borrower’s authenticity by conforming their identity. |

| Driving License | Driving license number | Name, DoB, Photo of licensee, Blood group, vehicle categories authorized to drive, Father/ Husband name, License validity, type & Issuing state | National Database for Driving Licenses and Vehicle Registration | Helps to know the vehicle details and acts as an address proof. |

| PAN | PAN number of the customer | Name, Address, and PAN validity | Database from National Securities Depository Limited and the Income Tax Department. | Helps to check if the borrower complies with tax regulations. |

| Voter ID | Voter ID number | Authentication, Name, Gender, Mobile Number, Email ID, DoB, Father/ husband name, Address, Polling booth, Parliamentary constituency | National Portal of India/Electoral Databases. | Helps to prevent identity fraud |

| OCR | Scanned image of any customer ID | Name, Father/ husband’s name, DoB, Face, Card Number | OCR technique | Reduces errors caused by manual inputs. Extracts data quickly and enhances document verification. |

| Passport Check | Passport number which is used to generate the MRZ code | Name, DoB, Age, Address, Passport type, expiration date | Passport Seva Kendra (PSK) Databases | Reliable proof to verify customer’s identity. |

| MCA | Company name or CIN (Corporate Identification Number) | Company details, directors, financial reports | Ministry of Corporate Affairs (MCA) | Verifies business run by borrowers by validating company registration details and financial compliance. |

| Electricity Bill Validation | Consumer ID and Name of the Electricity Service Provider | Address, Bill date, Latest bill amount, Due date, Email ID, Phone number, Payment arrears and Deposits | Regional State Electricity Board or the Authorized Electricity Supply Company of the state | Reliable address proof |

| LPG Connection Verification | LPG Customer ID (obtained from the bill). | Name, Address, Last four digits of registered Phone and Aadhar, Bank details, Bank details, Subsidy status, Number of subsidized refills consumed in the last year, Amount of subsidy availed, Total number of refills, Date since the previously generated bill, Distributor’s Name & Code | Regional State Electricity Board or the Authorized Electricity Supply Company of the state | Check and confirm residential information of the borrower. |